Material Insight: The Dielectric Constant of PCB Materials

Material Insight: The Dielectric Constant of PCB Materials American Made Advocacy: What About the Rest of the Technology Stack?

American Made Advocacy: What About the Rest of the Technology Stack? It’s Only Common Sense: Great Ideas From John Mitchell’s Book on Hiring Habits

It’s Only Common Sense: Great Ideas From John Mitchell’s Book on Hiring HabitsGlobal Notebook Shipments Forecast at Only 176 Million Units in 2023

November 3, 2022 | TrendForceEstimated reading time: 2 minutes

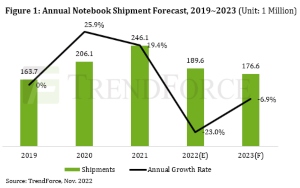

According to TrendForce, global notebook shipments in 4Q22 are likely to decline to 42.9 million units, down 7.2% QoQ and 32.3% YoY, lower than the same period before the pandemic. In addition, market demand is affected by negative factors such as inventory, the Russian-Ukrainian war, and rising inflation, leading to a downward revision of notebook market shipments in 2022 to 189 million units, a 23% decline YoY, with the proportion of shipments in the first and second half of the year at 53:47, the first top-heavy scenario in the past ten years.

According to research, the structural imbalance between notebook market supply and demand remains unresolved at present, leading this year's notebook shipments to present a downward movement trend quarter by quarter. TrendForce believes, after current inventory pressure gradually returns to a healthy level, Chromebooks may be the first wave of products that will see a recovery in demand by 2Q23 and traditional cyclical growth momentum is expected to return to the market, with shipments set to rebound slightly from 14.44 million in 2022 to 16.2 million units.

As mentioned above, pressure will continue in the consumer and commercial notebook market. Although demand for the former has been adjusting for five quarters, peak season momentum is still expected to play a major role. Coupled with assistance from the introduction of new CPUs, shipments of consumer notebooks will track closer to traditional peak season demand but declines will be inevitable throughout the year. Commercial demand faces dollar rate hikes leading to higher corporate borrowing rates and post-pandemic scenarios including capital expenditure adjustment, downsizing, and layoffs, which will cause an even greater decline than that of consumer notebooks.

In addition, although pandemic-induced demand has gradually weakening, hindering the growth of the high-end notebook market in 2022, TrendForce has observed that gaming and creator notebooks will remain cash cows. Facing the dilemma of the gradual decline in global notebook shipments, the high-margin nature of the segmented market has become more prominent. Major notebook manufacturers and processor brands such as Intel and Nvidia are all competing to expand, enhancing consumers’ user experience by means of high specifications and customization, while stimulating potential market demand to become a category of notebook computers capable of continual future growth.

However, inflationary pressure and geopolitics remain as variables in the general environment and the consumer electronics sector has borne the brunt of this uncertainty. The future shipment scale of the notebook computer market must still reference these relevant developments closely. In addition, considering that China continues to adopt a tough Zero-COVID policy after the 20th National Congress of the Communist Party of China and the adversarial relationship between it and the United States, supply chain strategies are also under scrutiny by major manufacturers. According to TrendForce research, due to the cumbersome and vast industrial settlement characteristics associated with notebook components, only major American manufacturers are currently promoting production development in Vietnam. Even though industrial chain reorganization to decouple from China has been in motion for some time, it still needs to be promoted by brands and ODMs in the short term.

As the global economy maintains course through battering headwinds, the International Monetary Fund (IMF) predicts that the 2023 economic growth rate will be approximately 2.7%, down 0.5 percentage points from 2022, which will be the most severe economic winter in 20 years. Overall, TrendForce estimates that there is no sign of obvious recovery in the global notebook market in 2023. Although the annual decline in shipments has abated to 6.9%, it will only reach 176 million units.

Share on:

Suggested Items

SPEA Expands in Southeast Asia with New Subsidiary in Thailand

05/17/2024 | SPEASPEA, a global leader in automatic test equipment for the manufacturing of semiconductor, microelectronic and electronic devices, today announced the opening of its new subsidiary in Thailand. This expansion marks a significant step forward in SPEA's commitment to serving the growing Southeast Asian microchip and electronics market with leading-edge manufacturing machinery and equipment.

PCB Market Size to Grow by $29.06B from 2024-2028

05/17/2024 | PRNewswireThe global printed circuit board (PCB) market size is estimated to grow by USD 29.06 bn from 2024-2028, according to Technavio. The market is estimated to grow at a CAGR of over 6.6% during the forecast period.

AT&S 2024/25 on Growth Course Again

05/17/2024 | AT&SAT&S operated in a challenging market environment in the financial year 2023/24. After a strong second quarter, demand was relatively weak again in some market segments in the second half of the financial year.

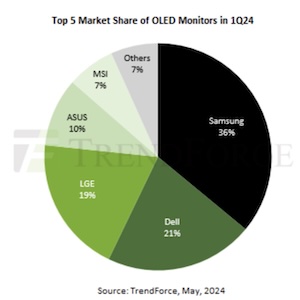

Shipments of OLED Monitors Hit 200,000 Units in 1Q24, Annual Forecast to Reach 1.34 Million

05/17/2024 | TrendForceTrendForce’s latest report reveals a robust start to 2024 for OLED monitors, with shipments reaching approximately 200,000 units in the first quarter—marking a YoY growth of 121%.

Magnachip Celebrates the Grand Opening of Magnachip Technology Company in China

05/16/2024 | MagnachipMagnachip Semiconductor Corporation celebrated the opening ceremony of Magnachip Technology Company, Ltd. (MTC) yesterday at its headquarters located in Hefei, China. MTC is a subsidiary of Magnachip, established on December 20, 2023, to expand the Company’s display driver IC and power IC businesses in China.