Material Insight: The Dielectric Constant of PCB Materials

Material Insight: The Dielectric Constant of PCB Materials American Made Advocacy: What About the Rest of the Technology Stack?

American Made Advocacy: What About the Rest of the Technology Stack? It’s Only Common Sense: Great Ideas From John Mitchell’s Book on Hiring Habits

It’s Only Common Sense: Great Ideas From John Mitchell’s Book on Hiring HabitsProjected YoY Growth Rate of Server Shipments for 2023 Has Been Revised Down to 2.8%

November 22, 2022 | TrendForceEstimated reading time: 2 minutes

Based on the latest data and research, TrendForce has further corrected down the projected YoY growth rate of whole server shipments for 2023 to 2.8%. Three factors are behind this revision. First, lead time has started to return to its usual length for most orders related to server components from 3Q23 onward. Seeing this, server OEMs and cloud service providers (CSPs) have also begun to correct the component mismatch issue by lowering demand for items that are in excess while maintaining a constant inventory level for items that are still in tight supply. This development, in turn, has reduced the flow of server orders going to ODMs. Second, the wave of demand that was generated earlier from the effects of the COVID-19 pandemic is dissipating. Hence, expansion activities have cooled off noticeably for services such as video streaming, e-commerce, etc. Among CSPs, Meta, Google, and ByteDance (TikTok) have lowered their server procurement quantities for next year. Lastly, the global economic outlook has remained fairly negative, so companies across most industry sectors have formulated a more conservative expenditure plan and scaled back IT-related spending for next year.

QoQ Declines in Prices of Server DRAM Modules and Enterprise SSDs for 4Q22 Have Widened to 23~28% as Competition Among Suppliers Intensifies

In the server DRAM market, DRAM suppliers are facing greater difficulties in raising sales because buyers have been carrying a high level of inventory during the second half of this year. In 3Q22, suppliers did manage to get some buyers to lock in the price for that quarter and the next .However, TrendForce believes that further downward corrections to next year’s server shipments have ratcheted up the price competition among suppliers. Moving into October, CSPs received even lower server DRAM quotes as suppliers proposed to lock in the price to the end of 1H23. Now, in November, another round of negotiations for “fourth-quarter special deals” has also commenced. Due to these developments, QoQ declines in contract prices of server DRAM modules for 4Q22 have enlarged to 23~28%.

Regarding the enterprise SSD market, orders remained relatively stable for a while. However, the increasingly conservative economic outlook and the downward revisions to corporate capital expenditure plans in 2H22 have led to softer demand momentum for enterprise SSDs. Moreover, NAND Flash suppliers face rising inventory for enterprise SSDs as the demand for consumer electronics has plummeted. Internally, they have been under pressure to find solutions for consuming excess production capacity and meeting their year-end targets. Externally, they need to prepare for headwinds such the expected weak demand situation during the low season of 1Q23 and delays in the production ramp-up of Intel’s and AMD’s new server CPU platforms. Given these factors, suppliers are compelled to offer larger price concessions on enterprise SSDs even though the contracts for this fourth quarter have already been arranged. Due to the new wave of negotiation activities, QoQ declines in contract prices of enterprise SSDs have exceeded the earlier estimation and now come to 23~28% as well.

Share on:

Suggested Items

Würth Elektronik in United States Embarks on New Milestone with State-of-the-Art Headquarters

05/17/2024 | Wurth ElektronikWürth Elektronik in the United States, a leading manufacturer of electronic and electromechanical components as well as custom magnetics, has announced the commencement of construction on a new 70,000-square-foot headquarters. This new facility underscores the company’s commitment to innovation and grow in the electronics industry.

Nortech Systems Reports Q1 Results and Actions to Reduce Facility Costs

05/17/2024 | BUSINESS WIRENortech Systems Incorporated, a leading provider of engineering and manufacturing solutions for complex electromedical and electromechanical products serving the medical, industrial and defense markets, reported first quarter ended March 31, 2024 financial results.

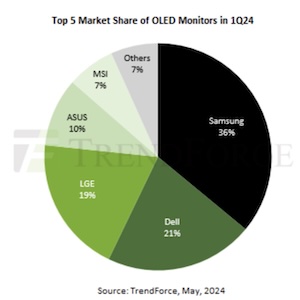

Shipments of OLED Monitors Hit 200,000 Units in 1Q24, Annual Forecast to Reach 1.34 Million

05/17/2024 | TrendForceTrendForce’s latest report reveals a robust start to 2024 for OLED monitors, with shipments reaching approximately 200,000 units in the first quarter—marking a YoY growth of 121%.

The ICAPE Group Reports Revenue for Q1 2024

05/16/2024 | ICAPE GroupThe ICAPE Group, a global technology distributor of printed circuit boards (PCB) and custom-made electromechanical parts, announced its revenue for the first quarter of 2024.

IDC: Indonesia’s Smartphone Market Starts the Year with a Strong 27.4% Growth in 1Q24

05/16/2024 | IDCIndonesia’s smartphone market grew sharply at 27.4% year-over-year (YoY) and 11.5% quarter-over-quarter (QoQ) to 10 million units in 1Q24, according to International Data Corporation’s (IDC) Worldwide Quarterly Mobile Phone Tracker.