The Right Approach: I Hear the Train A Comin'

The Right Approach: I Hear the Train A Comin' It’s Only Common Sense: OCCAM—the Time Is Now

It’s Only Common Sense: OCCAM—the Time Is Now Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing IndustryQ2 DRAM Industry Revenue Rebounds with a 20.4% Quarterly Increase

August 24, 2023 | TrendForceEstimated reading time: 2 minutes

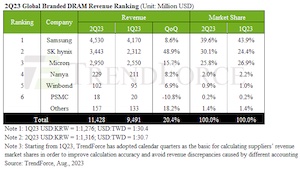

TrendForce reports that rising demand for AI servers has driven growth in HBM shipments. Combined with the wave of inventory buildup for DDR5 on the client side, the second quarter saw all three major DRAM suppliers experience shipment growth. Q2 revenue for the DRAM industry reached approximately US$11.43 billion, marking a 20.4% QoQ increase and halting a decline that persisted for three consecutive quarters. Among suppliers, SK hynix saw a significant quarterly growth of over 35% in shipments. The company’s shipments of DDR5 and HBM, both of which have higher ASP, increased significantly. As a result, SK hynix’s ASP grew counter-cyclically by 7–9%, driving its Q2 revenue to increase by nearly 50%. With revenue reaching US$3.44 billion, SK hynix claimed the second spot in the industry, leading growth in the sector.

Samsung, with its DDR5 process still at 1Ynm and limited shipments in the second quarter, experienced a drop in its ASP by around 7–9%. However, benefitting from inventory buildup by module houses and increased demand for AI server setups, Samsung saw a slight increase in shipments. This led to an 8.6% QoQ increase in Q2 revenue, reaching US$4.53 billion, securing them the top position. Micron, ranking third, was a bit late in HBM development. However, DDR5 shipments held a significant proportion, keeping their ASP relatively stable. Boosted by shipments, its revenue was around US$2.95 billion, a quarterly increase of 15.7%. Both companies saw a reduction in their market share.

Overall, due to the continued decline in contract prices for various products, suppliers continue to report negative operating profit margins. In Q2, Samsung’s operating margin improved from -24% to -9%. SK hynix witnessed simultaneous growth in revenue and ASP, narrowing its operating profit margin significantly from -50% to -2%. On the other hand, Micron’s operating profit margin improved slightly from -55.4% to -36%. TrendForce anticipates that the DRAM industry’s revenue will continue to grow in the third quarter. After suppliers reduce production, there’s a diminished inclination to drop prices, which means that contract prices are stabilizing, and future declines will be limited. As a result, the losses incurred from inventory price drops are anticipated to lessen, with operating profit margins expected to shift from losses to gains.

Nanya’s shipments have been declining for over four consecutive quarters. However, boosted by TV orders in the second quarter, its revenue increased by approximately 8.2%. Winbond’s revenue for the second quarter grew by 6.9%, primarily benefiting from the release of tenders in China and the added capacity from the KH factory, which has provided greater pricing flexibility, leading to an increase in order volume. PSMC primarily accounts for revenue from its in-house produced consumer DRAM products, excluding DRAM foundry services. Affected by subdued demand and a somewhat backward manufacturing process that lacks competitive pricing advantages, DRAM revenue declined by around 10.8%. This makes PSMC the only supplier with a decline this quarter. When factoring in DRAM foundry revenue, the decline stands at 7.8%.

Share on:

Suggested Items

NCAB Group Posts Interim Report Q1 2024

04/26/2024 | NCAB GroupNet sales decreased by 17% to SEK 950.6 million (1,146.4). Compared with the year-earlier period, sales were affected bylower prices and continued inventory adjustments by customers. In USD, net sales decreased 17%. For comparable units, net sales decreased 24% in both SEK and USD.

Amphenol Reports Q1 2024 Results, Announces New Stock Repurchase Program

04/26/2024 | BUSINESS WIREAmphenol Corporation reported first quarter 2024 results. In addition, the Company is announcing a new three-year, $2 billion stock repurchase program.

KLA Corporation Reports Fiscal 2024 Third Quarter Results

04/26/2024 | KLAKLA Corporation announced financial and operating results for its third quarter of fiscal year 2024, which ended on March 31, 2024, and reported GAAP net income of $601.5 million and GAAP earnings per diluted share of $4.43 on revenue of $2.36 billion.

Chinese Smartphone Market Maintains its Recovery Momentum at 6.5% Growth in 1Q24,

04/26/2024 | IDCAccording to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker, China smartphone shipments grew 6.5% year over year (YoY) to 69.3 million units in 1Q24.

Rogers Corporation Reports Q1 2024 Results

04/26/2024 | Rogers CorporationNet sales of $213.4 million increased 4.3% versus the prior quarter resulting from higher sales in the AES and EMS business units. AES net sales increased by 4.1% primarily related to higher aerospace and defense (A&D), wireless infrastructure, industrial and renewable energy sales, partially offset by lower EV/HEV and ADAS sales. EMS net sales increased by 2.8% primarily from higher general industrial, A&D and EV/HEV sales, partially offset by seasonally lower portable electronics sales.